International Institute for Middle East and Balkan Studies (IFIMES)[1] from Ljubljana, Slovenia, regularly analyses developments in the Middle East, Balkans and around the world. Maria Smotrytskais a senior research sinologist, specialized in the investment policy of China. In her comprehensive analysis entitled “European logistics hubs of Belt and Road Initiative. Aftermath of the BRI implementation in CEEC” she describeshow the CEE countries provide China with large platforms for investment and development of trade and economic collaboration.

International Politics & Economics specialist

The article describes the place and significance of the CEE region in the Chinese Belt and Road Initiative. Being a geopolitical bridge between Asia and Europe, the CEE countries provide the Chinese side with large platforms for investment and development of trade and economic collaboration. Main economic and infrastructural opportunities, provide by the BRI are analyzed in the article. Author comes to the conclusion of the position of the region in geopolitical map of the Chinese initiative.

Key words: BRI, CEE, Central and East Europe, China, 16+1, cooperation, opportunities

The second decade of the 21st century put the geoeconomic emphasis and cooperation within the framework of China's “One Belt, One Road” initiative into the China – East European states relations.

China's “One belt, One road” initiative today creates prerequisites for a significant increase in the geo-economic and geopolitical significance of the Central and Eastern European region (CEE), both for China and the European Union. Thus BRIinitiative, launched in 2013, “complements” existing national (Chinese) and European plans (for example, the so-called “Junker plan” or plans promoted by individual EU member States) to develop infrastructure and expand connectivity in Europe and beyond.

The Chinese initiative is dictated by the understanding of the importance of the CEE countries as an important component of a unified Europe. Thus, asserting itself in the role of one of the centers of a multipolar world order, Beijing began transforming the economic and political space that developed in CEE with the promotion of favorable economic proposals to the countries of the region, without raising questions of the difference of ideologies and ways of life.

For the first time, a joint project was announced in 2012 in Warsaw, where Premier Wen Jiabao launched an initiative called “12 measures” of China to encourage friendly cooperation with the countries of Central and Eastern Europe.

Starting in 2013, the main content of the programs of each 16 + 1 summit is the development of tools for this regional format. Naturally, the format of China's cooperation with the CEE countries is closely connected with the implementation of the global concept of the “New Silk Road” proposed by the Chairman of the PRC Xi Jinping. The concept consists of two parts: the land “Economic belt of the Silk Road” and the “Maritime Silk Road of the 21st Century” and potentially involves cooperation of at least 60 countries in Europe and Asia.

By 2015, China has become one of the largest investors in Eastern and South – Eastern Europe. In November 2015, the Eastern Europe - China (16 + 1) summit was held in the Chinese city of Suzhou, in which the leaders of the PRC and 16 Eastern European member states and the Balkan countries took part. The meeting resulted in the strengthening of China's economic presence in Eastern Europe. Also at the trade and economic forum in Hangzhou between China and the countries of CEE in 2015 it was agreed that China is ready to provide financial support for the re-industrialization of the countries of CEE, in the case that it will be conducted using Chinese technologies and equipment.

In 2015 – 2016, taking into account the opportunities and potentials, each country in the 16 + 1 format chose its own direction. For example, Bulgaria will supervise agriculture, Poland – investment and trade. The task of Latvia will be identification of links and projects, cooperation in the field of logistics, Romania will deal with energy projects, Lithuania is responsible for educational programs, and Hungary for the tourism sector.

The 16 + 1 format , in a certain sense, prepared the transition to a more focused and integrated strategy “One belt – One Road” and successfully “fits” into its main components – the projects “Economic belt of the Silk Road” and “Marine Silk Road of the XXI century”, aimed at developing new land and sea transport, logistics and trade and production systems linking China to Europe. In the first project, the countries of CEE play a key role, in the second – an important transit role in the development of “China – Europe” trade and investment ties, and in the long term – in the formation of a broad Eurasian “economic space” and “political stability belt”.

The basic design of the first project is the development on a new technological and organizational basis of the traditional direction of trade and transport “Sino – European” ties, complemented by their investment cooperation. This Northern road includes land international transit to Western Europe from China and other countries of the Asia – Pacific region (primarily, South Korea and Japan) through Russia and Kazakhstan along the Trans – Siberian Railway and the Kazakhstan railway with access to the European part of Russia in The Urals:

- Chengdu (Sichuan province) – Dostyk – Moscow – Brest – Lodz (Poland )

- Suzhou (Jiangsu province, Shanghai region ) – Warsaw (Poland )

- Chongqing (Sichuan region) – Duisburg (Germany)

- Zhengzhou (Henan, North China) – Hamburg (Germany)

- Wuhan (Hubei province, Yangtze belt region) – Pardubice (Czech Republic)

- Wuhan – Zabaikalsk – Hamburg

- Shenyang (Liaoning, Northeast China) – Hamburg

- Yiwu (Zhejiang, Shanghai region) – Madrid (Spain)

Nevertheless, the transit and logistical potential of the other CEE countries is still used slightly. Almost not involved in the “European part” of the Northern road are the ports of Poland and the Baltic countries that gravitate towards it. On the contrary, the main transport and logistics centers for Chinese goods (primarily German Duisburg and Hamburg) are already overloaded, and the possibilities for expanding their capacities are limited.

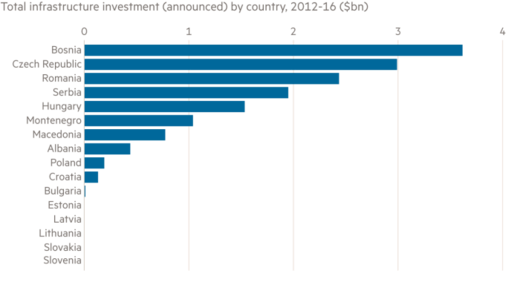

Such uneven distribution of cargo flows combined with insufficient technological level of the transport and logistics infrastructure of the CEE countries hinders the further development of China – Europe ties. There are also serious organizational and economic limitations of this development. Most of the provinces (especially the western ones, remote from the sea) tend to establish regular communication with Europe for both economic and prestigious reasons. The export potential of only the western provinces of China is estimated at $ 40 billion. Therefore, the full utilization of trains and partial financing of transportation costs are provided by local authorities on the basis of public – private partnerships (especially since many Chinese companies retain great state involvement) (see Figure 1 below).

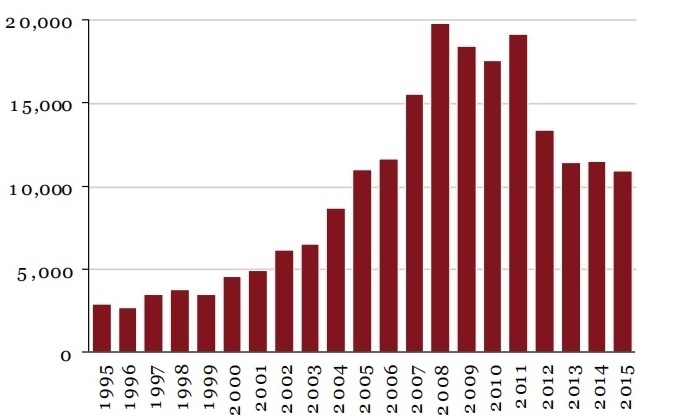

Figure 1.:China`s infrastucture investments in the 16 + 1

Source: CSIS; FT Research

The April 9th CEE – PRC summit 2019 in the Croatian city of Dubrovnik marked a new beginning in the development of relations between China and Eastern Europe. Although the Belt and Road initiative (BRI) usually focuses on Asian (whether Central Asian, South Asian, or South – East Asian) or African participants, post-Communist countries in Central and Eastern Europe have begun to play not less significant role. In fact, the CEE region was one of the most represented regions in the 2017 – 2019 BRI Forums: of the 28 heads of state or government, four were from this region (representing the Czech Republic, Poland, Hungary, and Serbia), and Romania was represented by a delegation led by the country's Deputy Prime Minister. This list of forum participants reflected the intensive development of cooperation between China and CEE under the auspices of the BRI.

Humanitarian influence is also increasing – the leadership of the PRC encourages interpersonal contacts with the CEE countries, especially through tourism, student and youth exchanges, etc. China's credibility in the region is also growing, because now almost any project of cooperation on a bi – versatile basis is served under the brand “One Belt – One Road”, which allows China to demonstrate real (albeit small) successes literally every year. This is especially noticeable against the backdrop of crisis phenomena in the European Union and the weakening of the ties between the CEE region and Russia.

Underlining the main opportunities of BRI for CEE and EU, should be mentioned the following:

Other interviewees considered that rail services would attract demand mainly from shipping rather than from air. One of them, responsible for air cargo services, argued that rail would not abstract demand from air because it could not offer the very short transit times required by the most time-sensitive air cargoes. This interviewee also suggested that, to remain competitive, China and other parts of Asia with rail services introduced as a result of the BRI would still need air freight connections to Europe. In this context, ownership of the capacity of a cargo airline such as Cargolux can be seen as a key element of the infrastructure connecting China and theEU. A representative of the Community of European Railway and Infrastructure Companies (Hereinafter CER – Auth.) agreed that rail would attract demand from shipping but would not be able to compete with air services. The European Commission also suggested that, from China’s perspective, the maritime elements of the BRI were more important and that overland rail was a maritime and would remain so. This is broadly consistent with the analysis of maritime and air traffic. It should also be stressed that the most common investments by Chinese parties in the EU appear to be ports, principally in the Mediterranean and the United Kingdom.

Russian Railways (Hereinafter RZD – Auth.) has long operated rail services along the Trans – Siberian Railway between Europe and the Sea of Japan. These could, in principle, be used to carry goods from Japan and South Korea to Europe, but these would first have to be shipped across the Sea of Japan to Russia. In contrast, from landlocked north east China, long overland journeys are needed to reach any port, but may also be needed to reach a suitable railhead.

Thus, the commercial objective of growing rail services appears not to be to put pressure on maritime operators, which are already efficient, but to offer a higher speed service. This also helps producers and consumers along the rail routes used.

One interviewee in the logistics sector said that subsidies granted by the Chinese Government to rail services between China and the EU are “tremendous”. They also stated that Kazakhstan Railways (Hereinafter KTZ – Auth.) had reduced tariffs in 2012 but now agreed with RZD to keep tariffs high. KTZ indicated that the Chinese Government provided subsidies to support westbound container traffic, but envisaged that these would be withdrawn by 2020 as balancing eastbound traffic was attracted to the route. These comments illustrate a number of issues relating to the commercial viability of the services.Also trains between China and the EU will be charged transit tariffs by operators such as KTZ and RZD. There is no uniquely correct basis for setting such transit tariffs, although the principal applied in the EU is that they should be based on marginal costs. From the perspective of these transit railways, however, transit traffic is an opportunity to profit from third parties (A similar issue emerges in the provision of air navigation services within the EU, where national air navigation service providers (Hereinafter ANSPs – Auth.) may have incentives to overcharge for en-route services provided to overflying, and typically foreign, aircraft to subsidise terminal services provided to aircraft taking off and landing). The incentives on the transit states are typically to maximise their profits, rather than to maximise the economic, social and environmental value of the railway operation as a whole. For both the EU and China, however, there is the potential risk that a growing and successful rail service will be seen as a potential source of profit by the transit railways.

Figure 2 and Figure 3 below summarise the volumes of loaded containers which are loaded and discharged on flows between ports in the Far East and ports in the EU, measured in TEU. However, the EU Member States in which containers are loaded and discharged may not be the final destination states (The country where custom controls are executed is the country of discharge. This is the reason why Czech Republic is included in Figure 5 below despite it has not access to the sea.)

Figure 2 below illustrates the recent growth in loaded containers from the Far East to EU ports, from just over TEU one million in 1996 to about TEU eleven million in 2016. Other than China, no state loads more than one million containers to Europe.

Figure 2.: Loaded containers from the Far East to Europe: country of loading

Source: MDST World Cargo Database

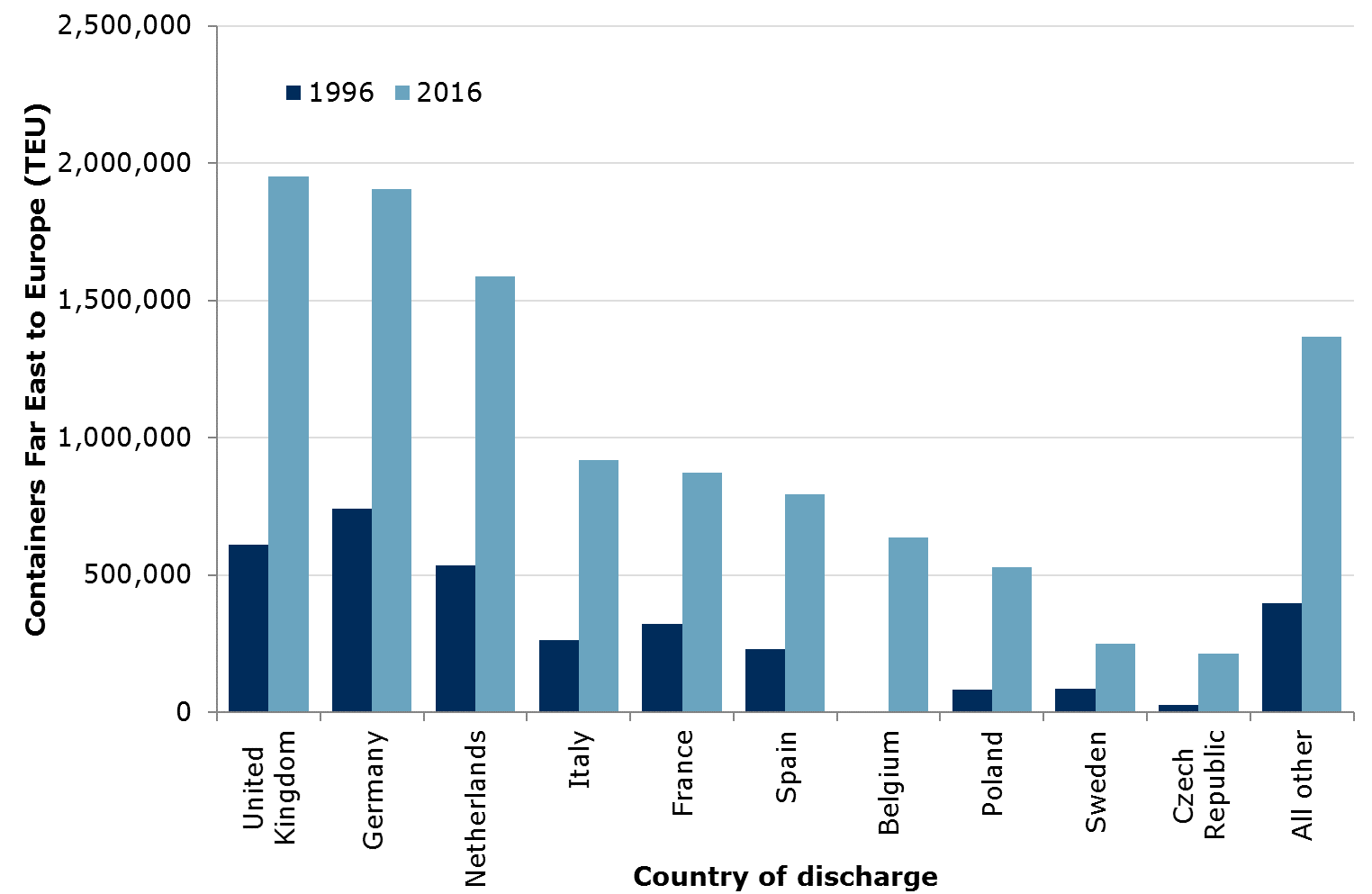

Figure 3shows the points at which loaded containers are discharged in the EU. A large proportion are discharged at ports in the United Kingdom, Germany, the Netherlands and Italy, before travelling onwards to the points at which they are stripped. Containers discharged in Rotterdam in the Netherlands, or Genoa (Genova) or Trieste in Italy, for example, may continue by river barge, train or truck to other EU Member States or to landlocked and non-EU Switzerland.

Figure 3.: Loaded containers from the Far East to Europe: country of discharge

Source: MDST World Cargo Database

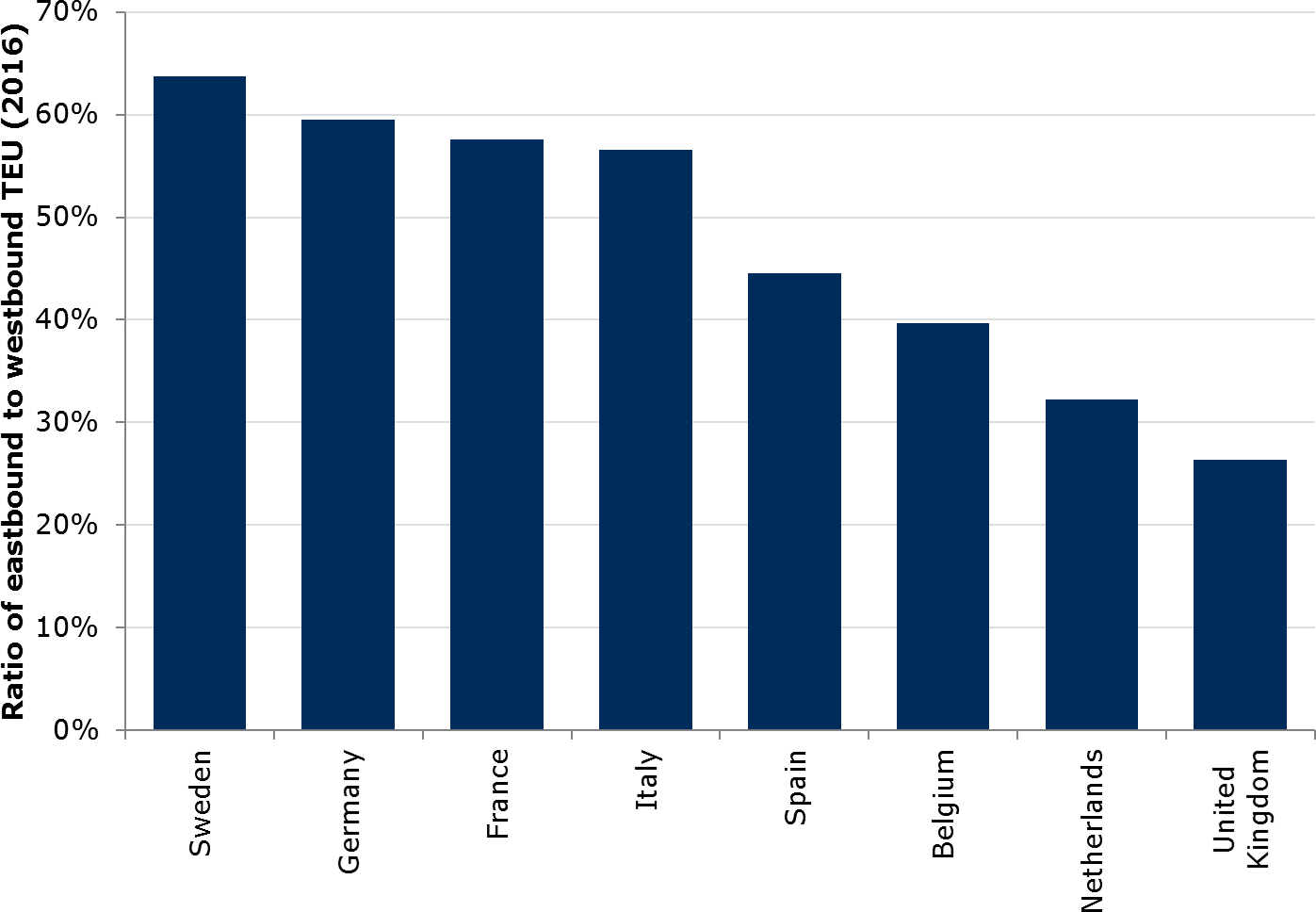

Thus, the analysis of Figures 2 and 3 and 4 show that westbound loaded container flows of 11 million TEU exceed the eastbound flows of 5 million TEU. This creates a need for a large number of containers to be returned empty in the eastbound direction. A representative of the CER said that this represented an opportunity for the EU to rebalance imports and exports.

Of the Member States shown, the largest imbalance in flows is for the United Kingdom, which exports only just over one quarter as many loaded TEUs as it imports. Even in Germany and Sweden, exports are less than two thirds of imports. This appears to confirm CER’s view that additional containers could be carried eastbound, in principle at little additional cost.

Figure 4.: Balance in loaded container flows for selected EU Member States

Source: MDST World Cargo Database

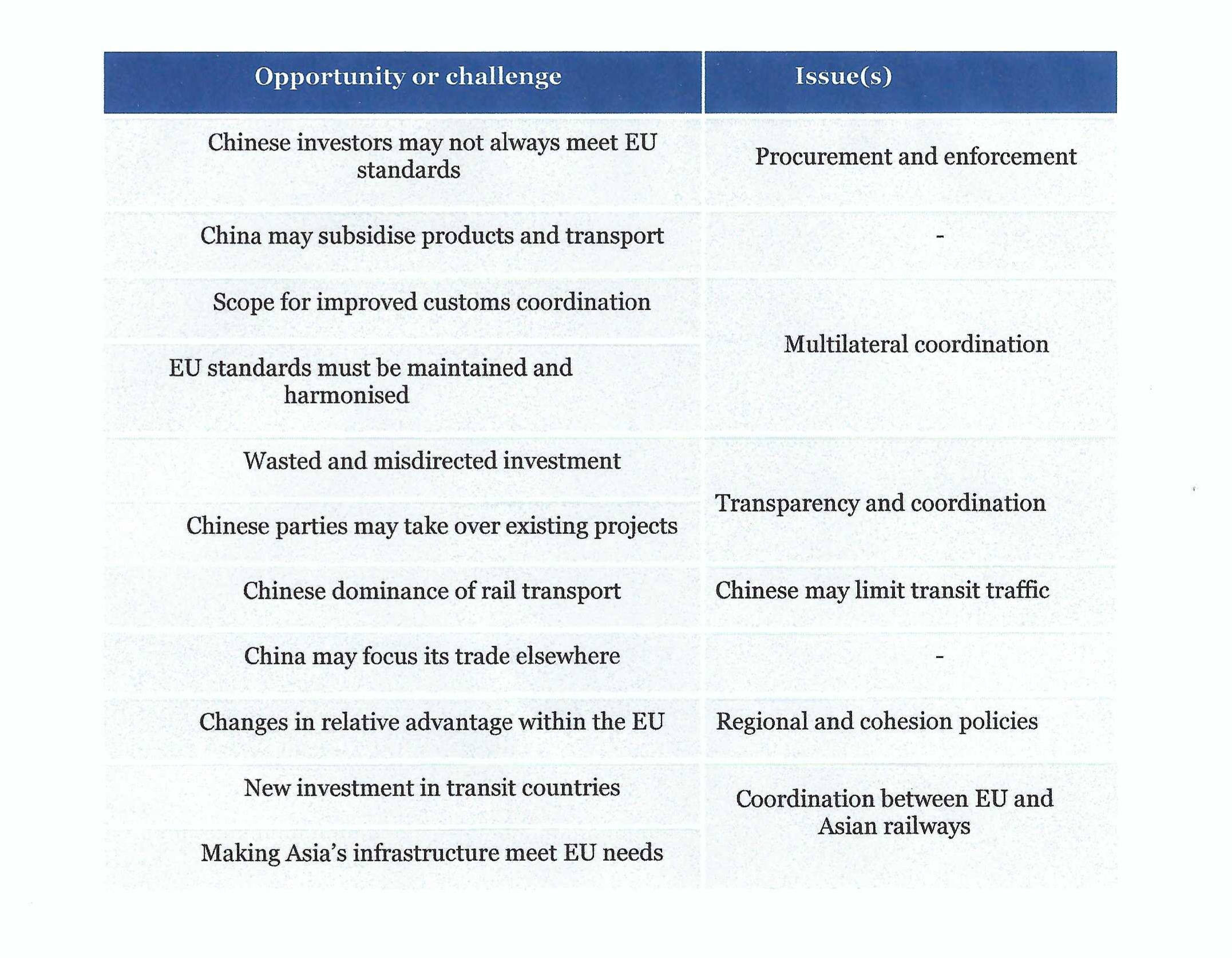

Table 1below summarises a number of the opportunities and challenges which appear to emerge from the BRI. None of these may amount to a clearly-defined “problem”, as outlined in the EC’s Better Regulation Toolbox. Nonetheless, this section briefly discusses the extent to which it might be relevant to consider legislation to address them.

Source:Steer Davies Gleave analysis

Thus, it can be noted that the participating countries of 16 + 1 mechanism understood the scale, prospects and synergies of this interaction. It should be emphasized that the “Old” EU countries are wary of Chinese activity in the Central European zone of their influence and insist that all members (and candidate members) coordinate their cooperation with China, and that the EU should speak with the PRC “with one voice”. Nevertheless the strategic concepts of the development of these states reflect the importance and priority of both bilateral relations with China and cooperation in the China – EU format. That is why most of the foreign policy strategies of the CEE states are oriented toward expanding foreign economic activity and trade with the PRC. It is necessary to emphasize the consistency and planning of work in this direction, conducted by the states of the 16 + 1 format. As we can see, pragmatic economic diplomacy started to prevail in the newest foreign policy history of Europe.

Analyzing the role of CEE countries in the implementation of the BRI, it should be emphasized that the created by China 16 + 1 initiative is an inter-regional cooperation in which China focuses on linking its efforts with those of Europe and considers rail links, ports and foreign direct investment as the basis for ensuring balanced development and social cohesion in European countries. For example, the construction of a railway between Hungary and Serbia was far more important for both countries than obtaining short-term economic benefits. It is part of an Express route connecting land and sea from the port of Piraeus across the Balkan Peninsula to the main corridor in Europe. In the future, the Express route will be extended to cover new areas near the three seas that wash the coasts of the CEE countries.

Thus it can be traced thee goal of China's cooperation with Central and Eastern European countries is not to continue to use CEE countries as a trade route, but to combine the industrial development needs of these countries with China's large production capacity, using the potential of Central and Eastern European countries in the Chinese market. If Chinese products are close to the Central European market, it is necessary to ensure the presence of high-tech products from CEE countries in the Chinese markets.

Today we can see that the main benefit, which CEE region can gain from its` participation in the BRI – the opportunity to boost the development of infrastructure of the region and improve region logistics.

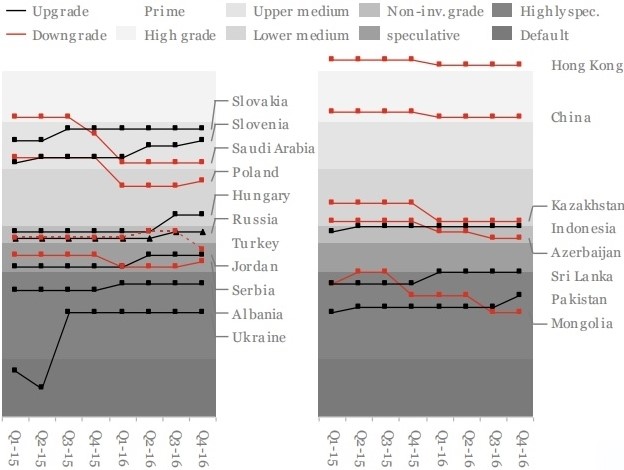

Thus, a lot of European and Chinese think-tanks, despite the few downgrades, noted that the BRI sovereign debt environment is not destabilized. Figure 1 below shows Europe had some downgrades on the back of political instability 2015 – 2016 (Turkey, Ukraine and Poland), but was more upbeat overall. Russia also was upgraded from BB+ negative to Stable in September 2016.

Figure 1.: Sovereign rating reassessments: Europe & Asia

Source.: Standart and Poor`s, PwC proprietary research

Considering infrastructure as a key factor for competitive growth in CEE, should be mentioned that the inadequate infrastructure supply creates a growth barrier in the region. Thus European business leaders still believe that an inadequate infrastructure is a substantial barrier to business growth in the CEE.

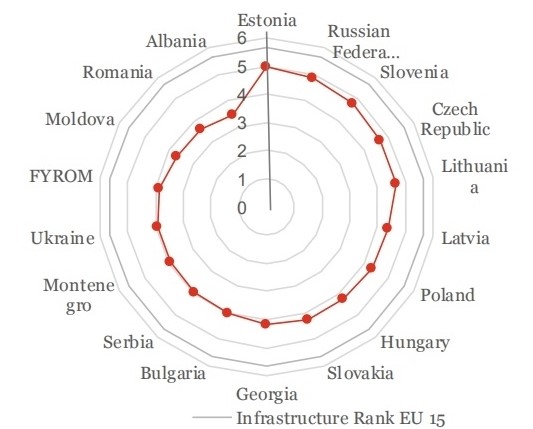

Figure 2 below shows that CEE ranks significantly lower in the infrastructure index than Western Europe. Also figure shows that infrastructure is the 4th most significant barrier for growth in Bulgaria and 7th in Poland and Romania. Thus, it is worth noting that Poland is the world`s 36th most competitive country, ranks only 53th when it comes to infrastructure.

Figure 2.: GCI (2016/2017) : Infrastructure ranks in CEE:

Source: WEF, PwC proprietary research

It can be seen that with the support of EU, CEE infrastructure has significant progress to date, and there is still ground to cover. Figure 3 below shows that Almost EUR 210 bn has been spent on transport infrastructure in CEE EU Member States over the past 20 years. This equals to over EUR 100 spent per capita in each year. Over EUR 150 billion has been spent from EU Structural Funds only. Additional money made available from the Connecting Europe Facility and the European Investment Bank who invested almost EUR 30 billion in transport in CEE over last 10 years. European Fund for Strategic Investment (part of Junker Plan) plays increasingly important role in CEE – by mitigating risks and offering attractive financing.

Figure 3.: Infrastructure investments in the EU 11 (EUR million):

Source: OECD, PwC proprietary research

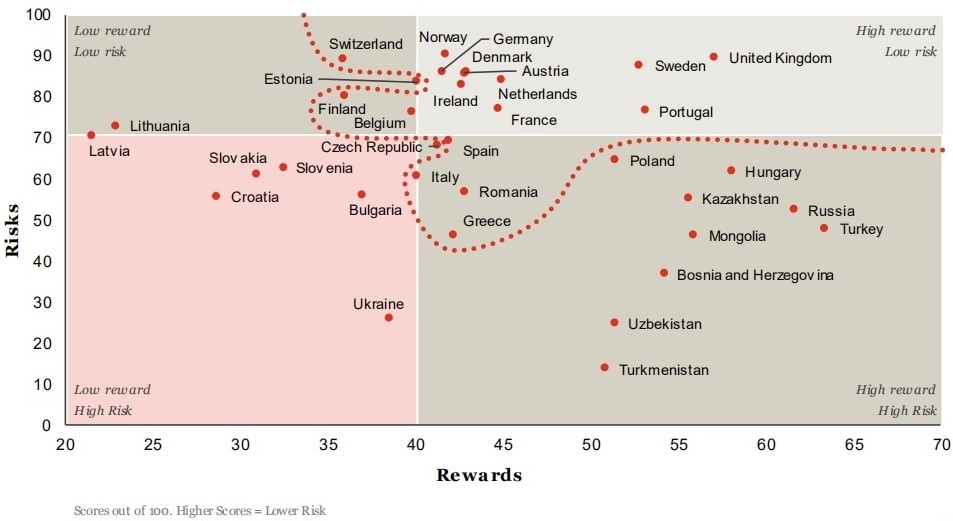

Thus, CEE region is land of opportunity, but there is still the balance of risk and reward. Figure 4 below shows that CEE risk / reward balance is generally less attractive than in Western Europe. This figure makes it clear that CEE countries will have to compete with Western European economies, which are generally perceived as more attractive. Still, the scarcity of “ready-to-finance” infrastructure projects globally and the enormous liquidity awaiting investment opportunities might play in favour of CEE, provided there is a pipeline of well-prepared projects, and risks are mitigated.

Figure 4.: Infrastucture Risk-Reward Index

Source: BMI Risk, PwC proprietary research

It can be traced that CEE is expected to outpace Western Europe over the next 5 years with construction market growth of 3.1%. The Figure 5 below shows that CEE is expected to outpace Western Europe over the next 5 years with construction market growth of 3.1%。This creates good opportunities for domestic and international companies and investors.

Figure 5.: Construction Market Growth

Source.: European Commission

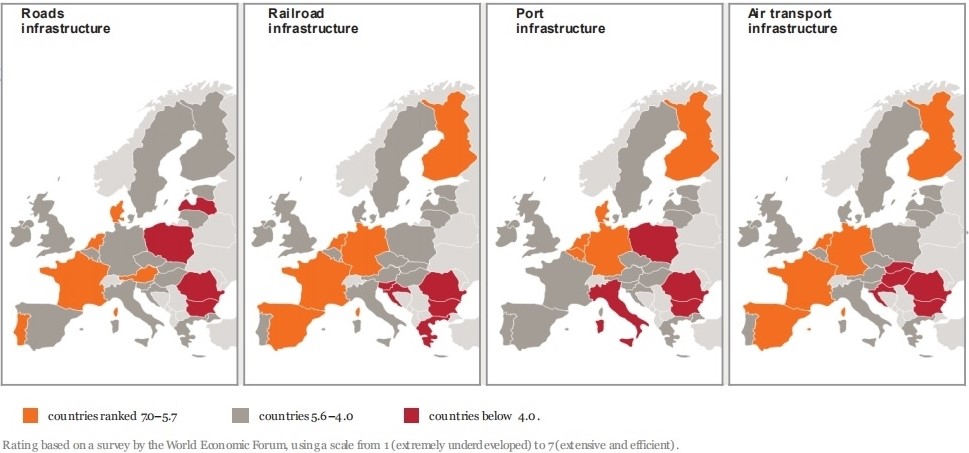

However, CEE needs further investments to reach the EU15’s level of competitiveness. The Map 1 below makes it clear that after decades of under-investment, ploughing money into new routes and modernising and maintaining the existing transport system across the region remains crucial for achieving sustainable economic growth and maximising the region’s competitive potential.

Map 1.: Quality of transport infrastructure:

Source: World Economic Forum

Analysing the logistic of the BRI in Europe, Map 2 below shows that of the six economic corridors outlined in the BRI initiative, the most relevant for CEE and the rest of Europe is the New Eurasian Land Bridge, which connects China to Europe via Central Asia, past Russia and through to the Netherlands. China plans to strengthen connectivity and speed up freight transport along this route.

Map 2.: Proposed roads of the BRI:

Source: PwC proprietary research

It is also worth noting the issue of stabilization of subsidies for infrastructure and logistics projects of the PRC through the EU – Asia line.

Thus, the average amount of subsidies varies by region and is $3500 – 4000 per FEU, with the tariff level for transporting a container from China to Europe about $9000; taking into account the subsidy, it is reduced to $5000. A similar estimate is given by another think-tank: about $5,000 for transporting a container by rail from Chengdu to Hamburg (see Table 1 below). In general, regional subsidies range from $1,500 to $7,000 per FEU. It turns out that this de facto subsidy allows you to “reset” the transportation fee on Chinese territory.

Table 1.: EU – Bound Container Traffic Subsidies Provided by Regional Chinese Authorities, Effective Years and Average Subsidised Through Freight Rates

Source.: in-house estimates

The data presented above makes it clear that the BRI initiative offers new opportunities to broaden and deepen trade and investment cooperation between China and CEE. Moving from being export destinations to becoming investment partners in production, technology, finance and infrastructure development, the CEE countries are likely to see new trade patterns emerge with China.

Also it should be noted that CEE regions acts as a very convenient logistics hub for China. Thus, being a geopolitical bridge between Asia and Europe, the CEE countries provide the Chinese side with large platforms for investment and development of trade and economic collaboration.The CEE region has the advantage of location: overland shipments from Western China via Russia or Central Asia are routed to Western Europe. Thus, China gains a strategic advantage from redistributing some of its Maritime supplies, reducing the use of the Strait of Malacca. In addition, there are commercial considerations: 1) in terms of time, this overland route speeds up transportation twice as compared to the usual way of delivery by sea with reloading to the railway, and 2) in terms of price it is much more profitable than air transportation.

Today it can be seen that the cooperation with the countries of Central and Eastern Europe, which are located along the transport routes of both the SREB and the MSR, has become one of the most priority directions of China's foreign policy in Europe in recent years. The CEE countries, faced with a difficult relationship with Brussels with a financial deficit, technological backwardness of infrastructure and a decrease in export volumes in the 2000s, perceive interaction with China as a chance for their economic development.

Presented and advertised as compatible and complementary to any regional project, the BRI is now becoming a very effective mechanism for creating “satellite” projects, such as the 16 + 1 platform. It should be mentioned that the 16 + 1 format was perceived by the Chinese side as a regional project that corresponds to the goals of the BRI, aimed at broader economic cooperation that goes beyond infrastructure. Thus, in addition to the economic relationship between China and CEE, which was considered the main direction of cooperation, the 16 + 1 platform in its structure and design embodied strong political and diplomatic potential ties.

The ninth summit of cooperation between China and CEE, based on the results, was the last for the 16 + 1 format. In April 2019, it became clear that Greece would be invited to be part of this initiative. This actually turns 16 + 1 into 17 + 1. This move confirms claims that the importance of the CEE countries to China is closely linked to COSCO's acquisition of a controlling stake in the Greek port of Piraeus. With this strategy, Beijing is partly paving the way for a resolution of the dispute between Greece and Macedonia, aiming to connect the port of Piraeus via Macedonia to the proposed high-speed rail link between Belgrade and Budapest, and then direct it to the Western part of the continent.

The appearance of 17 + 1 has a direct bearing on the cooperation between China and CEE. Greece's accession is likely to weaken some regional aspects of cooperation between partners and re-emphasize the bilateral nature of China's relations with individual countries. This is a strategic step that will bear fruit for both Beijing and the CEE capitals, and will also aim to allay EU fears that China is trying to split the continent.

The potential development of the 17 + 1 initiative demonstrates that China has already become a full-fledged “European power”. The growing number of Chinese investments and relations on the continent suggests a much broader and more complex “deepening” into European Affairs than expected by Beijing or any European capital. This reality requires China to own its position as a “European power”. At the same time, Europe needs to engage in a mature and meaningful debate about the growing influence of China's power, which goes beyond simplistic divisions between friend / foe, rival / ally, and so on. As the evolution of cooperation between China and CEE shows, that we live in a complex world and interlocutors can simultaneously perform several contradictory roles. Due to the BRI initiative, Europe has realized that it is impossible to sacrifice China, and ignoring the fact that this country has become the “new power of the European continent” can cause significant damage to the Union, primarily economic.

About the author:

Maria Smotrytskais a senior research sinologist, specialized in the investment policy of China; BRI-related initiatives; Sino - European ties, etc. She is distinguished member of the Ukrainian Association of Sinologists. She has PhD in International politics, Central China Normal University (Wuhan, Hubei province, PR China)

Ljubljana/Shanghai, 29 November 2020

Footnotes:

[1] IFIMES – International Institute for Middle East and Balkan Studies, based in Ljubljana, Slovenia, has Special Consultative status at ECOSOC/UN, New York, since 2018.

[2] The Central Asia Regional Economic Cooperation (Hereinafter CAREC – Auth.) Program is a partnership of 11 countries (Afghanistan, Azerbaijan, China, Georgia, Kazakhstan, Kyrgyzstan, Mongolia, Pakistan, Tajikistan, Turkmenistan, and Uzbekistan) and 6 multilateral development partners (Asian Development Bank, European Bank for Reconstruction and Development, International Monetary Fund, Islamic Development Bank, United Nations Development Programme, and World Bank) working to promote development through cooperation, accelerate economic growth, and reduce poverty. ADB serves as the Secretariat .